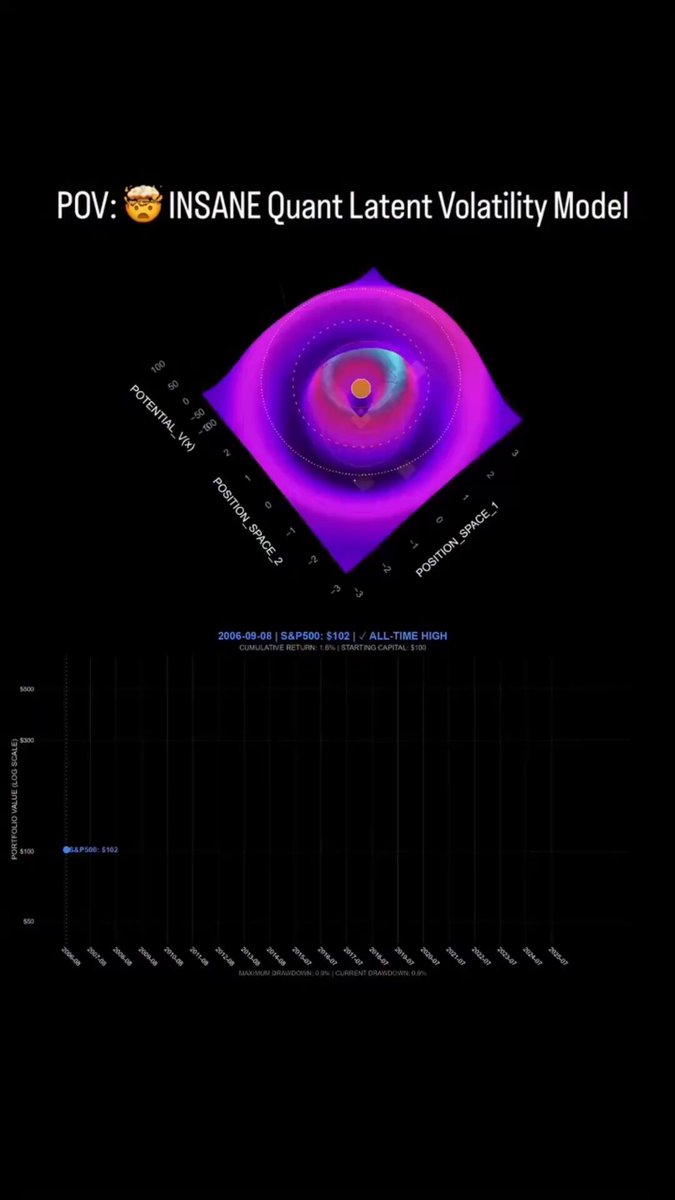

程序员利用 OpenClaw 构建量化模型分析标普 500 波动率结构以预测市场不稳定。

投研分析📅 2026/03/15

#API#Crypto#手动触发#中风险#可复用#半自动#交易员#报告#美股#行情数据

A Programmer Built a Quant Model with OpenClaw that Analyzes the S&P 500. Not the price. The volatility structure behind it. The model maps a 3D "risk surface" of the market. When the peak shifts away from equilibrium… Large market moves often follow. So I asked OpenClaw what was actually happening in this video. It explained the structure behind the model. A trader on Polymarket appears to be using something similar. Look at the account above. $75K profit and 107 predictions. Mostly S&P 500 markets. But the system isn’t predicting direction. It’s detecting when the market becomes unstable. The structure Claude described looks like this: > map the latent volatility surface of the market > detect shifts away from equilibrium > reduce exposure before volatility shocks > re-enter once the system stabilizes Just volatility structure. Sometimes the real edge in markets… is seeing instability before it shows up on the chart.